The Independent Investment Management Initiative (IIMI), a member-led industry group that represents specialist investment firms, has just welcomed its 50th member. The think tank which has seen a 43% increase in membership over the past 12 months, has welcomed 15 new members in the past 12 months. These include 49th member, sustainability start-up Rebalance Earth founded by Robert Gardner’s (co founder of Redington and mallowstreet), and its 50th member CG Asset Management, which manages the FTSE 250 listed Capital Gearing Trust, among other funds.

Dani Hristova, Chief Executive Officer for IIMI, commented: “The growth of our membership signals the importance of our collective voice within the asset management ecosystem. I’m also delighted that, as we have grown, our membership has diversified further. We now support more businesses that provide critical infrastructure and services to boutiques for example, ACDs and distribution partners. The regulatory, operational and commercial headwinds for smaller firms remain disproportionate and I’m proud that through our collective efforts, we’re able to ease some of these pressures and help firms to thrive. It’s imperative that investment specialists compete alongside global asset managers so that we can increase investment choice and ensure good client outcomes”.

Chris Taylor, Chief Operating Officer of CG Asset Management said: “We are delighted to become IIMI’s 50th member, especially at a time when independent firms are playing an increasingly vital role in the investment landscape. IIMI’s work in championing the interests of specialist firms like ours is invaluable, and we are eager to contribute to the collective effort. It’s crucial that boutique managers have a voice in shaping regulation and ensuring a competitive market, so that we can continue to deliver the best outcomes for our clients.” About the Independent Investment Management Initiative: The Independent Investment Management Initiative (IIMI) is a member-led industry think tank representing specialist, entrepreneurial investment boutiques that are entirely focused on and aligned with the interests of their investors.

Founded in 2010, the IIMI counts amongst its 50 members some of the world’s leading specialist asset management firms, overseeing over c. $640bn in client assets and representing c. 3,000 members of staff. Over the past two decades, as the financial services industry has been dominated by global giants, an increasing appreciation of a traditional ‘client-centric’ approach has enabled entrepreneurial firms in the UK and beyond to emerge as a growing competitive force. The IIMI offers these firms an expert voice in the debate over best practice and the future of financial regulation, with the aim of building a better future for smaller and independent asset managers that prioritise specialism over scale in delivering the best results to clients. The IIMI has three core aims: to shape a regulatory environment that supports boutiques and promotes competition, to promote the strengths of boutiques and facilitate commercial opportunities for members, and to drive best practice across our membership.

For IIMI press enquiries, please contact: Sam Emery, Quill PR: sam@quillpr.com 07798 881 770 Emma Murphy, Quill PR: emma@quillpr.com 07872 604 413

The guiding principle of IIMI is that boutiques are beneficial for the entire ecosystem of asset management within the UK. They facilitate greater diversity of investment options, competition, and specialisation that ultimately benefit investors. In tandem we also focus our efforts on trying to ensure that these small companies, whose structures are often designed to facilitate relatively easy setup and nimbleness, are also fit for purpose when protecting their clients, employees and partners. The purpose of this paper is to review the corporate structures which many IIMI members have adopted – highlighting their merits whilst cognisant of potential pitfalls – and to help inform decisions around choice and evolution in corporate structures”.

IIMI members are comprised of several different corporate structures. See figure 1. For a chart of those in Limited Liability Partnerships vs Limited Company Structures.

Over the last decade, attitudes towards ESG and sustainability within asset management have transformed irrevocably.

Triggered by investor and regulatory demand, fund managers are incorporating ESG into their investment processes and objectives in ever greater numbers. For example, PwC predicts that ESG-related AuM (assets under management) at investment firms will increase by 12.9% annually from $18.4 trillion in 2021 to $33.9 trillion by 2026 – totalling 21.5% of all global AuM.

The rapid growth of ESG and sustainable investing does, however, present challenges which the funds industry needs to address. Within this, boutique firms face particular risks and opportunities.

Greenwashing

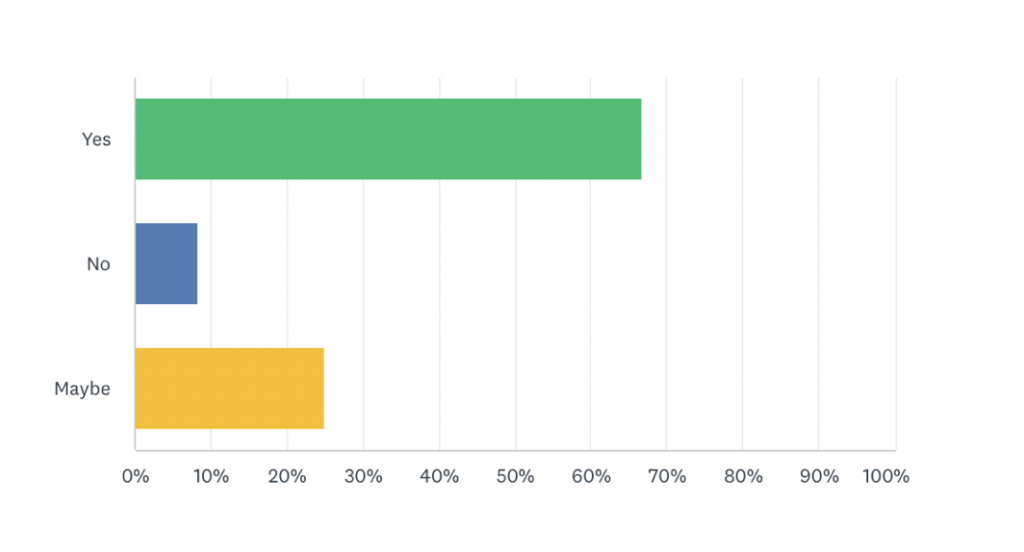

Much has been written about both the mis-selling of ESG and the exaggerated claims being made about sustainability (a.k.a. greenwashing) by the asset management industry. A survey of ESG experts within IIMI’s diverse membership revealed that 66% believed greenwashing is a major problem for the industry.

Is Greenwashing a major problem for the funds industry?

Regulators agree with this sentiment. In a Dear CEO letter penned by the UK Financial Conduct Authority (FCA) in 2021, the regulator gave several examples of ESG-focused funds whose ESG credentials it believed were somewhat questionable.

For instance, one so-called sustainable investment fund, said the FCA, had substantial exposure to high-emitting energy companies, yet did not seem to be undertaking any stewardship activities (e.g. by encouraging the companies to transition to net zero). If such behaviour is allowed to go unchecked, investor trust in ESG and sustainability funds will be eroded.

Regulators across the globe have woken up to this risk. Just as MiFID II (Markets in Financial Instruments Directive II) sought to prevent managers from selling risky products to unsuitable retail clients, the regulation is once again being updated to ensure that clients are asked about their sustainability preferences before being put into the most appropriate funds.

As well as introducing new regulations, the authorities have taken action against managers whose ESG conduct has fallen below expectations. In 2022, the US Securities and Exchange Commission (SEC) fined the asset management arm of Goldman Sachs $4 million for policy and procedural failures around its ESG research. Prior to this, BNY Mellon was struck with a $1.5 million fine from the SEC for allegedly misstating and omitting information about ESG across some of its mutual funds.[1]

With regulators putting managers’ ESG credentials under the spotlight, boutique firms should exercise caution when making claims about ESG or sustainability. Managers also need to clearly articulate their ESG or sustainability objectives to clients, so as to avoid any confusion.

Too many cooks spoil the broth

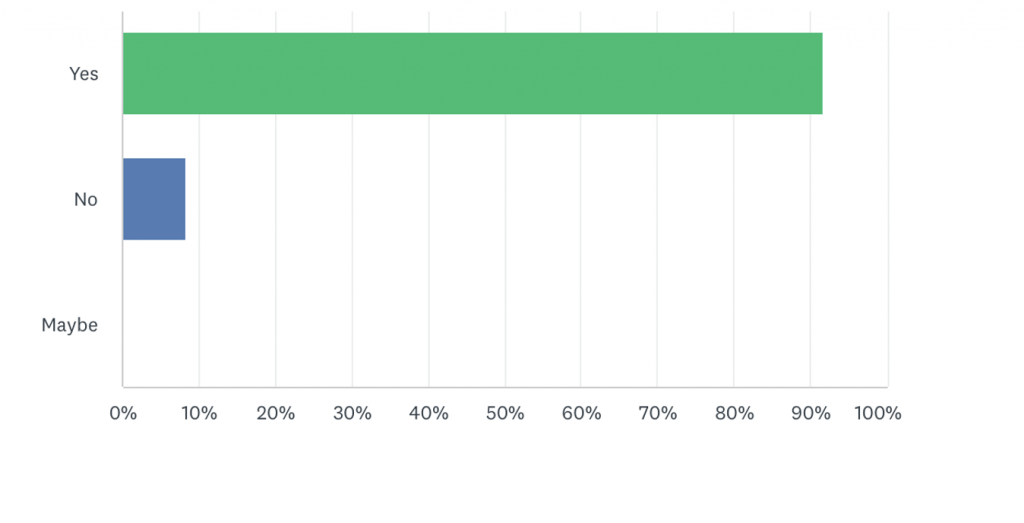

Although many regulators have made progress on ESG regulation, the lack of alignment and dialogue between the different market supervisors is a problem. Again, this deficiency is recognised by IIMI’s membership. Ninety-one percent of IIMI members complained that ESG/sustainable finance regulations are too fragmented across different jurisdictions.

Do you think that ESG/sustainable finance regulations are too disjointed across different jurisdictions?

Take what is happening in the EU and UK. Whereas the EU has imposed the SFDR (Sustainable Finance Disclosure Regulation), the FCA is consulting on the SDR (Sustainable Finance Disclosure Requirements). As these names imply, both sets of rules are designed to strengthen the underlying transparency of sustainable investment products and funds, but there are nuances between what the UK and EU are doing.

For example, the UK’s SDR is a labelling regime and it is not adopting some of the more restrictive provisions contained in the EU’s SFDR, such as mandated templates and the “do not harm principle”.[2] Furthermore, the EU’s SFDR allows for a so-called ‘light green’ (article 8) disclosure, whereas the FCA has a higher bar for sustainable funds. Inconsistencies of this kind between different markets’ ESG regulations risks saddling asset managers with added costs at a time when their margins are already being challenged.

It is clear the authorities need to become more consistent in terms of how they supervise ESG and sustainable investing. A failure to do so will result in confusion prevailing at investment firms and their clients. To mitigate this risk from happening, the funds industry should play a more proactive role, and engage with global regulators about the importance of having harmonised rules in place for ESG.

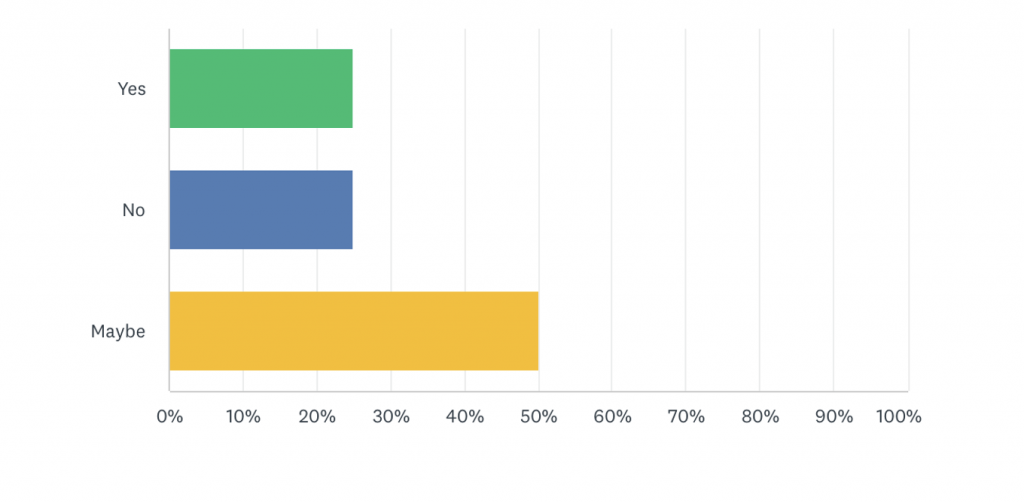

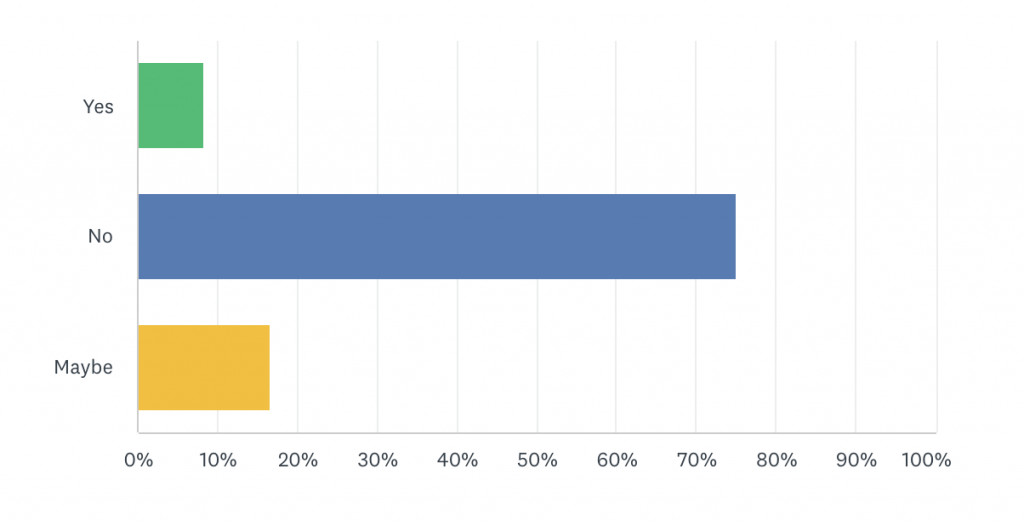

Nonetheless, IIMI members are relatively bullish that regulations will eventually facilitate inflows into sustainable investments. Twenty-five percent said regulations would definitively drive inflows, while 50% reckoned such rules would ‘maybe’ lead to more investment in sustainable assets.

Will regulations lead to substantial inflows into sustainable investments over the next few years?

Dealing with the political fallout on ESG

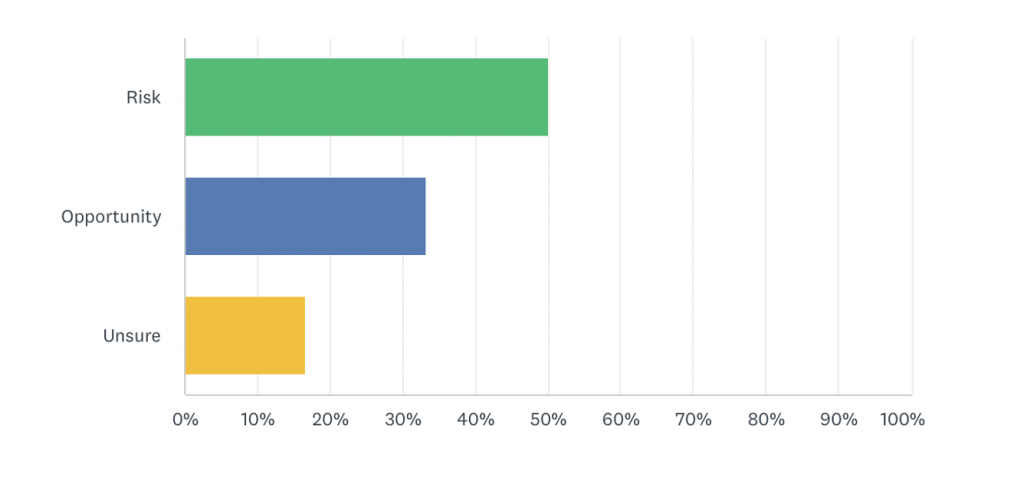

The politicisation of ESG is a risk that some asset managers are saying could impede their ability to raise funds, especially in the US. According to a survey of IIMI members, 50% described the anti-ESG movement as a risk facing their businesses.

Do you see the anti-ESG movement as being more of a risk or opportunity for your business?

So what is happening?

Hostility against ESG investing – dubbed ‘woke capitalism’ in some circles – is rising, with more than a dozen Republican-leaning US states introducing legislation aimed at limiting or even prohibiting ESG investing by public pension plans. Some of these states have even forced government pension funds to divest from money managers which take into account climate change or race issues when investing.

More recently, House Republicans voted to block Labor Department proposals allowing pension funds to consider ESG when investing and exercising shareholder rights through proxy voting.

Combating ESG hostility among policymakers is something asset managers should be thinking about, but they must approach the matter sensitively. The industry needs to tread carefully on this issue because a large chunk of its AuM is derived from US institutions in states where these rules are being enforced.

Although it is sensible for regulators to encourage investors to consider ESG when making decisions, banning or severely constraining allocators from making ESG investments altogether restricts choice, and with it the ability to obtain new sources of returns and achieve proper diversification. The funds industry needs to reach out to policymakers – especially those which may be anti-ESG – and articulate the strategic value of having ESG or sustainability-linked holdings in investment portfolios.

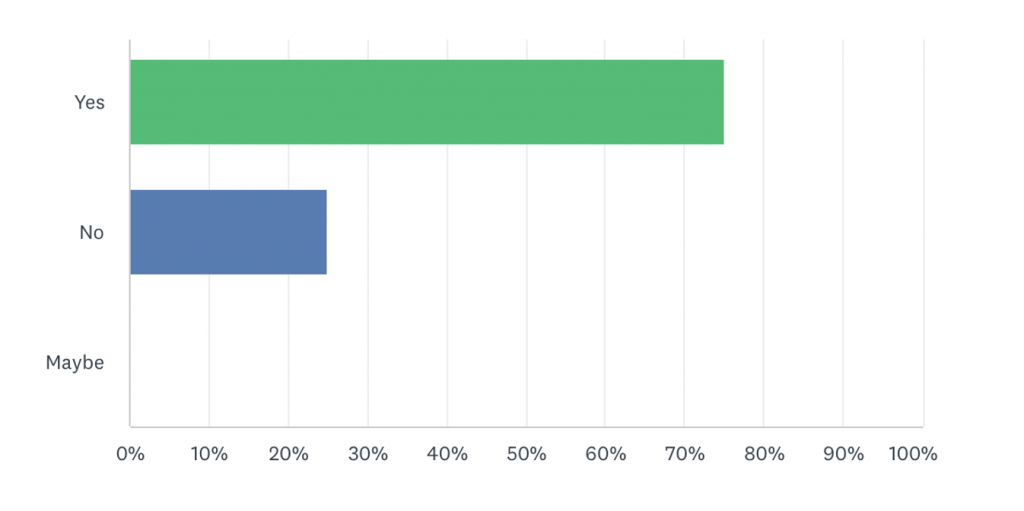

Elsewhere, the war in Ukraine has also created challenges for ESG investors, as fossil fuel companies have outperformed a number of other industries and sectors. Despite concerns that responsible investing would fall by the wayside as a result of the boom in fossil fuels, 75% of IIMI members said the war in Ukraine was not having an impact on their approaches to responsible investment.

Has the war in Ukraine changed your approach to responsible investment?

Addressing new ESG paradigms

Asset managers must ensure that they stay up to speed with the various changes shaping ESG and sustainable investing.

Right now, there are growing concerns that some asset managers are not paying adequate attention to biodiversity, following a report by ShareAction, an NGO, which found just 10% of managers have a dedicated biodiversity policy in place covering all of their portfolios, while 40% of firms do not monitor whether their investee companies operate in areas of biodiversity importance.[3]

Moreover, the number of funds focusing exclusively on biodiversity is very low. According to Morningstar, there are just 14 funds collectively managing $1.6 billion, which target biodiversity as an investment theme.[4]

These findings come not long after the COP 15 Agreement pledged to reduce biodiversity losses by protecting 30% of land and sea by 2030. Post-COP 15, biodiversity risk is something which investors (and regulators) are starting to take seriously. If asset managers are to demonstrate to institutional clients that they are fully on top of ESG, they will need to develop policies outlining how they are navigating biodiversity risk, and develop strategies off the back of it.

IIMI members are themselves starting to pay closer attention to biodiversity risk, with 75% noting this is an area which they will be devoting more resources to over the course of 2023, with 44% saying this is being driven by client demand, and a further 33% by risk mitigation.

Will you be spending more time on biodiversity risk in 2023?

A blueprint for augmenting ESG in asset management

Despite the challenges facing ESG and the wider market more generally, ESG investing has proven resilient. However, it is critical that asset managers do not become complacent, otherwise appetite for ESG and sustainable funds could decline.

So what do managers need to do?

As greenwashing becomes more of a problem, asset managers will need to overhaul their communications with investors on ESG, by providing more evidence-based and granular reporting outlining how they are meeting their ESG targets and goals.

Similarly, a more robust engagement strategy is needed with regulators to counter some of the fragmentation and rising anti-ESG sentiment.

Having focused extensively on how to reduce their carbon footprints, asset managers need to start concentrating on biodiversity risk, as this is currently top of mind for policymakers, regulators, and increasingly investors.

If fund managers can achieve these goals, then the ESG market will flourish moving forward.

[1] Financial Times – November 22, 2022 – Goldman Sachs to pay $4m penalty over ESG fund claims

[2] Bovill – December 21, 2022 – SDR and SFDR – uncomfortable bedfellows

[3] Bloomberg – February 26, 2023 – Asset managers found to have blind spot around new ESG risk

[4] Morningstar – December 5, 2022 – Biodiversity – what should we expect from COP15?

Introduced in July 2022, the UK’s Financial Services and Markets Bill (FSMB) is a landmark piece of post-Brexit legislation, which could usher in some potentially significant changes to how the domestic financial services industry – including asset management – is regulated.

The FSMB is looking to bolster the competitiveness of the UK on the global stage. The Bill will implement outcomes of the Future Regulatory Framework, support the Government’s levelling up agenda, and also aims to harness the opportunities of “innovative technologies” in financial services.

At the heart of the FSMB, which may become law by as early as Spring 2023, is a proposal which could see the revocation of all retained EU laws related to financial services, including UCITS, AIFMD (Alternative Investment Fund Managers Directive), MiFIR (Markets in Financial Instruments Regulation), Solvency II and the PRIIPs (Packaged Retail and Insurance-based Products) rules, along with regulations covering sustainability related disclosures, derivatives and short selling

However, it is important to stress that revocation does not necessarily mean these rules will be scrapped entirely – if at all – although they might be subject to changes.

Why is this happening?

At the point at which Brexit was consummated, the UK onshored vast swathes of pre-existing EU laws, mainly because there was no domestic legislation to replace them. A lot of the onshored rules are prudent and relatively uncontentious, so will likely be retained. However, there might be EU laws which are duplicative of UK legislation or that are no longer suitable given the UK is no longer in the Single Market. Meanwhile, some laws may simply be inappropriate and in need of annulment.

The rules certainly create scope for the UK’s financial services regulations to diverge from the EU. For instance, the UK government has already said it will try and use these powers to impose changes to MiFIR, including removing the UK share trading obligation together with revisions to the rules around pre-trade transparency and systematic internalisers.

More significantly, the UK has already said it will implement substantial changes to the Solvency II regime, aimed at insurance companies. Under the revised rules, insurers will be subject to lower risk margin requirements and could benefit from streamlined reporting. If these provisions are enacted, the Treasury believes £100 billion of trapped capital in the insurance industry could be freed to invest into illiquid assets, including long-term infrastructure programmes and green energy.

In some quarters, however, there are mounting concerns that the FSMB could result in asset managers operating in both the UK and EU having to comply with two different sets of rules, a scenario which could create cost and complexity at a time when the industry needs neither.

Nonetheless, there is certainly potential for UK regulators to revise some of the existing rules as they apply to funds. IIMI will be reaching out to its diverse membership to discuss if any particular aspects of EU funds law needs changing, the findings of which will be outlined in a white paper later in Q1.

2022 was a particularly bruising year for asset managers, with many portfolios being adversely impacted by a combination of market volatility and soaring inflation. Experts already anticipate that 2023 will be tougher, as firms implement aggressive cost-cutting measures to stave off revenue decline and further fee compression.

Amid these difficult headwinds, the industry will need to deal with a plethora of incoming rule changes and potential regulatory developments.

So what awaits fund managers on the horizon?

Further scrutiny of ESG is inevitable

Allocations to ESG or sustainable funds remained relatively healthy in 2022, in contrast to the heavy withdrawals seen elsewhere. According to Morningstar data, sustainable funds drew in $22.5 billion in Q3, whereas the wider industry suffered outflows totalling $198 billion. [1] Despite the asset class’ resilience, regulatory scrutiny of ESG funds is expected to intensify in 2023 as the authorities look to root out greenwashing and product mis-selling.

This comes not long after a series of regulatory fines were levied against several high-profile managers for various ESG shortcomings. In 2022, the US Securities and Exchange Commission (SEC) fined the asset management arm of Goldman Sachs $4 million for policy and procedural failures around its ESG research. Prior to this, BNY Mellon was hit with a $1.5 million fine from the SEC for purportedly mis-stating and omitting information about ESG across some of its mutual funds. [2]

With regulators putting managers’ ESG credentials under the spotlight, boutique firms will need to exercise caution when making investment claims about ESG or sustainability. Conversely, this could also be an excellent opportunity for smaller firms – which are typically more specialised – to communicate clearly to prospective investors about what they are doing around ESG.

Expect some divergence between EU and UK regulations over time

Introduced in July 2022, the UK’s Financial Services and Markets Bill (FSMB) proposes a number of changes to existing UK financial services regulation, as the country attempts to usher in greater competition post-Brexit.

Among the provisions contained within the Bill include the revocation of retained EU law as it relates to financial services set out in Schedule 1, including the rules implementing the Alternative Investment Fund Managers Directive (AIFMD), the Markets in Financial Instruments Regulation (MIFIR) and UCITS. [3] Other upcoming differences include the regulation of sustainable finance, with different disclosure, marketing and naming standards emerging out of the UK and the EU.

This, however, does not mean the UK will jettison EU regulations overnight. Firstly, the government has stressed that there will be no revocation of existing EU rules unless there is a domestic law to replace it. Additionally, experts point out the government will be reluctant to deviate excessively from EU laws, preferring instead to tailor or finesse the rules.

Nonetheless, managers should brace themselves for the possibility of some regulatory divergences between the UK and EU moving forward, although the full impact of this is still yet to be determined.

Prepare for settlement compression

From March 2024, equities traded in the US and Canada will be settled on a T+1 basis instead of T+2, and other markets will likely follow suit (In fact, India began phasing in T+1 in 2022).

Although T+1 could help generate capital efficiencies, there are some unresolved issues, which need clarifying. Firstly, there are concerns about whether financial institutions based in different time zones to the US will need to pre-fund some of their trades. Under the existing T+2 model, financial institutions have two days after the trade date to settle their FX transactions, but under T+1 organisations would need to book FX trades on either the same day or T+1.

While this change will be felt most acutely by financial market infrastructures (i.e. CSDs) and custodians, asset managers could face challenges as well. A move to T+1 may lead to fund managers suffering from an increase in trade fails, resulting in additional costs. If these are to be avoided, it is vital that managers ensure their operational processes and in-house systems can handle the imminent T+1 transition.

Accordingly, asset managers should engage with providers this year about how best to prepare for the T+1 rollout in North America and beyond.

[1] Financial Times – January 3, 2023 – Robust inflows obscure a difficult year for ESG funds

[2] Financial Times – November 22, 2022 – Goldman Sachs to pay $4m penalty over ESG fund claims

[3] Simmons & Simmons (July 22, 2022) Financial Services ands Markets Bill Introduced to Parliament

Black swan events can and do happen as COVID-19 has shown. As a result, investors are increasingly demanding assurances from asset managers that they have robust contingency plans in place to deal with all sorts of crisis situations. Top of mind right now is the prospect of looming energy shortages in Europe this winter, and what it could mean for business continuity at asset managers.

This comes amid growing concern that European governments – including here in the UK – could be forced to cut power networks for short periods if Russian gas supplies are further constricted. Such outages will likely hinder managers’ ability to trade, a scenario which could have serious consequences, especially if markets are volatile.

So what tangible steps are firms taking in Europe to minimise the risk of energy disruption on their business operations?

A number of financial institutions – including banks and asset managers – have been drafting up contingency plans to deal with the possibility of energy shortages. According to Bloomberg, some organisations are looking to learn from experiences in South Africa, a country whose businesses have been forced to deal with rolling blackouts for over a decade now.

Most asset managers have plans in place to either leverage regional disaster recovery sites or encourage staff to work remotely should London (or any other financial hub in Europe) suffer prolonged power outages. In many instances, these contingency plans will not be that dissimilar to what firms did during the beginning of the pandemic.

A handful of larger financial institutions have said they could relocate staff to different countries if a particular market suffers an acute energy emergency. For example, JP Morgan recently confirmed that it has plans in place to temporarily transfer employees from Europe to the UK or US in the event of severe energy shortages and blackouts on the continent. Given their relative size, this is not an option available to most boutique fund managers.

Some financial institutions are also looking to install backup diesel generators – which can provide up to three days’ worth of uninterrupted power – or even solar panels, at their offices and employees’ homes, to offset the risk of blackouts. This is something that boutiques ought to be actively considering.

In addition, asset managers should be conducting due diligence on their own critical service providers – including global custodians and fund administrators – to validate that they have solid contingency plans in place to deal with any outages.

And finally, asset managers should be thinking about ways they can reduce their own energy consumption. Such simple measures could include things like installing a smart meter, using less air conditioning or heating; and turning off the lights at night. Not only could these initiatives help mitigate the risk of blackouts if done collectively, but it will enable asset managers to reduce costs and burnish their ESG (environmental, social, governance) credentials.

With rolling energy blackouts a real possibility in Europe this winter, asset managers need to make sure that they have well-thought-out contingency plans to deal with this risk.

ESG (environmental, social, governance) and sustainable investment approaches are being integrated more extensively into the strategies of asset managers. According to PwC estimates, ESG-related assets under management (AUM) could reach $33.9 trillion by 2026, an increase from $18.4 trillion last year.[1] Amid this growth, however, greenwashing has become a real problem within the industry and one that threatens its credibility.

Some regulators – including the EU and now the UK FCA (Financial Conduct Authority) – want to tighten the rules on managers making sustainability claims, and require them to specifically define their goals and methods around sustainable investing.

For instance, the FCA is looking to clamp down on managers mislabelling their funds as being green while simultaneously creating a framework to support investors when looking for sustainable funds.

So how will the FCA go about this?

Firstly, the FCA is proposing three separate labels for funds – ‘sustainable focus’, ‘sustainable improvers’ and ‘sustainable impact’.

There will also be restrictions on how certain sustainability-related terms such as ‘green,’ ‘ESG’ or ‘sustainable’ can be used in product names and marketing for products which do not qualify for the sustainable investment labels. The FCA also added managers should make additional disclosures to clients who want more information about a product’s sustainability.

This comes not long after the FCA wrote a “Dear Chair” letter, in which the regulator described some of the more egregious instances of asset managers making unsubstantiated claims about sustainability to investors.

For example, the FCA observed that one purportedly sustainable investment firm contained two high carbon emissions energy companies in its top 10 holdings, without providing any context or rationale behind it (i.e. a stewardship approach that supports companies moving towards an orderly transition to net zero).

The FCA is the latest regulator to clamp down on greenwashing. The EU is widely considered to be one of the most advanced markets when it comes to ESG having introduced the SFDR (Sustainable Finance Disclosure Regulation) and the Taxonomy for sustainable economic activities.

The US is starting to take a tough line on managers misrepresenting their ‘green’ credentials as well. Earlier this year, the US Securities and Exchange Commission (SEC) announced plans to target asset managers with misleading fund names, by demanding firms prove that 80% of their holdings match the names given to their funds. In other words, if a fund has green in its title, then 80% of its underlying assets should be green.

The SEC is also recommending that funds and advisers provide more specific disclosures about their strategies in prospectuses, annual reports and adviser brochures. In the case of managers who claim to be making an environmental impact, they will be required to publish the greenhouse gas emissions associated with their underlying portfolio investments.

ESG and sustainable investing have been littered with challenges, not least because some managers have made spurious claims about sustainability. One of the reasons why this has been allowed to happen is the lack of regulation in the new market.

Although new regulation is welcome – if it improves standards and safeguards investors against miss-selling it is vital that there is a degree of harmonisation between what different market supervisors are doing in terms of their policies – otherwise it risks sowing confusion, and undermining the industry’s push towards ESG and sustainable investing.

IIMI will be looking to provide feedback to the FCA on these proposals. As part of this, IIMI will be gathering the opinions of its members, particularly those in the IIMI ESG Network. Any correspondence or opinions on this issue should be sent by IIMI members to the executive committee.

[1] PwC – October 10, 2022 – PwC’s Asset and Wealth Management Revolution 2022 Report

With the US now set to reduce its trade settlement cycle for equities from T+2 to T+1 beginning in March 2024, asset managers in the UK need to start thinking about how this change could impact their operations.

Why asset managers should take note of the move to T+1

Pushed for initially by SIFMA (Securities Industry and Financial Markets Association), the ICI (Investment Company Institute) and the DTCC (Depository Trust & Clearing Corporation) following the market pandemonium caused by COVID-19 and the meme trading escapade, the SEC (Securities and Exchange Commission) finally gave its backing in February to shortening equity settlement times from T+2 to T+1.

By narrowing the time it takes to settle a trade by a whole day, regulators argue it will help mitigate settlement and counterparty risk during the transactional process, curtailing the need to post as much margin on trades, and ultimately allowing for capital to be freed up, and deployed elsewhere, generating surplus liquidity. The US’s transition to T+1 is something which many financial institutions – including asset managers – largely welcome, at least from a balance sheet perspective

Confronting the challenges of settlement compression

Although T+1 could help generate capital efficiencies, there are some unresolved issues, which need clarifying. Firstly, there are concerns about whether financial institutions based in different time zones to the US will need to pre-fund some of their trades. Under the existing T+2 model, financial institutions have two days after the trade date to settle their FX transactions, but under T+1 organisations would need to book FX trades on either the same day or T+1.

A move to T+1 could also lead to fund managers suffering from an increase in trade fails, resulting in additional costs or even fines. If penalties for settlement fails are to be avoided, it is vital that managers ensure their operational processes and in-house systems can handle T+1.

Another risk which needs avoiding is market fragmentation. Not all markets will move to T+1 simultaneously raising the prospect of having a multiplicity of different trade settlement times in various markets. Not everyone is convinced that fragmentation of this sort will be a problem though. Asset managers, for instance, have a long track record of operating in markets where trade settlement times are not harmonised, so the US’s move to T+1 should not be particularly onerous for them.

Is anyone else following in the US’s footsteps?

The US is not the only market adopting T+1. India is already phasing in T+1, while Canada is poised to introduce T+1 at the same time as the US. A handful of emerging markets (especially those whose equity markets are closely tied to the US) have also indicated they could eventually move to T+1, although it is still early days.

Experts – speaking during an AFME (Association for Financial Markets in Europe) Conference in London, recently said that Brexit could potentially enable the UK to take a lead on embracing T+1, ahead of the EU. Nonetheless, the appetite for T+1 in the EU is fairly limited (although not non-existent), especially following the trading bloc’s laborious implementation of T+2 several years earlier.

With settlement times likely to change across more markets, asset managers should think about how this could affect their core operations.

It has been well over a decade now since the early social media pioneers (i.e. LinkedIn, Facebook) first started integrating themselves into the world of financial services. However, their arrival was not welcomed initially by everyone – including compliance departments at asset managers, who became increasingly alarmed at the regulatory and legal risks, which these online platforms posed.

In contrast to corporate email accounts or mobile phones, private correspondence conducted via social media could not be monitored – making it hard for firms to spot incidences of insider trading or other inappropriate communication exchanges. Almost immediately, a number of investment firms drafted up strict policies governing the use of social media by staff, with many dictating that any official communications between colleagues themselves or with prospective or existing clients should only be carried out through authorised channels (i.e. company email accounts and work phones, and not social media platforms or personal devices).

This exact same problem is once again repeating itself today.

Over the last few years, the use of private messaging tools such as WhatsApp – often on personal devices – has become increasingly ubiquitous in the workplace. There are several reasons for this. In the aftermath of the 2008 crisis, a number of financial institutions engaged in aggressive cost cutting programmes, with some even asking employees to use personal mobile phones for work purposes, a policy which resulted in more people – intentionally or otherwise – leveraging private messaging apps for business reasons.

It was the pandemic, however, that had the most dramatic effect as the introduction of remote working forced staff to rely more on their personal devices and private messaging apps for communication purposes.

Consequentially, the ability for firms to accurately monitor and document internal and external communications has diminished thereby increasing the risk of deliberate or inadvertent compliance breaches. Regulators are taking note of this deficiency.

Even before COVID-19 struck, regulators including the Securities and Exchange Commission (SEC) had been probing banks about the controls and recordkeeping arrangements they had in place over employees’ personal devices. The SEC has since fined a number of leading banks more than $1 billion collectively over failures to keep proper records of employee communications conducted on personal mobile devices. Data regulators are also examining whether sensitive information is being relayed and stored on private messaging platforms – amid concerns that General Data Protection Regulation provisions are being violated.

In response, nearly all banks have now imposed a blanket ban on staff conducting official business on private messaging apps such as WhatsApp. So will asset managers follow banks in restricting these private messaging apps?

It is looking increasingly likely that they will, not least because one major European asset manager has already confirmed it will be setting aside $12 million to cover any potential regulatory fines linked to its employees’ use of personal devices and recordkeeping arrangements.

In terms of next steps, some investment firms intend on formally banning staff from using private messaging tools or personal devices for work purposes. Others are purchasing technology systems which allow them to monitor employee conversations carried out on WhatsApp, together with other communication channels like Zoom and Microsoft Teams.

This is an issue which the funds industry needs to address urgently, especially as regulators are likely to extend their scrutiny beyond just the banks.

Tokenisation – namely the conversion of real assets or financial instruments – into digital tokens which are traded on a Blockchain – is making waves in the funds’ industry.

This is because tokenisation can also be applied to fund shares or units. The concept of tokenisation is something which industry bodies – including the Investment Association (IA) – are urging UK regulators to get on top of.

But what is driving this interest exactly, and is it something the FCA (Financial Conduct Authority) ought to consider?

Proponents of tokenisation argue the practice can facilitate faster settlement, reduce counterparty risk by displacing a number of intermediaries in the investment chain, improve transparency during the transactional process, and supports fractional ownership.

In theory, fractional ownership of fund units or shares would make it much cheaper and easier for investors to gain exposure to a fund, versus buying directly into one. From an allocator perspective, this would democratise investment.

Similarly, asset managers also have a lot to gain from tokenisation – assuming it is implemented correctly.

By making the investment process less outmoded and manual, tokenisation could help managers win mandates from millennials and Generation Z investors, a retail demographic which has largely avoided putting money into traditional funds, often preferring instead to engage in day trading or speculating on unregulated products such crypto-currencies.

This could allow managers to widen their investor footprint enabling the industry to grow AUM share further and future proof their businesses.

It is hard to fault the merits of tokenisation in this particular instance.

While tokenisation could bring a number of opportunities to the traditional funds industry, there are some areas where IIMI believes it might pose challenges.

Tokenisation’s advocates have repeatedly said that fractionalisation will open up private markets and other illiquid assets to retail clients by lowering minimum investment thresholds and boosting secondary market activity. This – they argue – will unlock a lot of liquidity, which is currently trapped in the private markets.

But should private markets be open to retail investors?

IIMI is of the view that private markets ought to be the domain of institutions only. Irrespective of whether they are fractionalised and the amounts of money involved are nominal, private markets are complicated in nature and unsuitable for retail.

Moreover, there are mounting concerns that liquidity mismatches could emerge in tokenised versions of private markets. If retail clients do suffer losses or are unable to redeem cash from tokenised versions of the private markets, then this could cause irreparable damage to the tokenisation cause as a whole.

IIMI is conducting a survey of its membership on digital assets, with the aim of producing a white paper later in the year. We encourage the membership to participate in this survey.

We use cookies to improve your experience on our website - read our Cookie Policy

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.